Hugh Grant plans to tear down new Swedish home

What's the first thing you do after snapping up a luxury six million kronor ($704,000) villa in Sweden, with sea views, two kitchens and a fireplace? If you're Hugh Grant: you raze it to the ground.

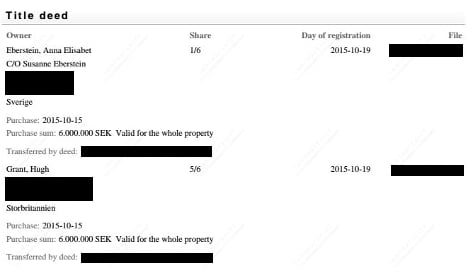

The Local was last week able to reveal official paperwork confirming that the Hollywood actor had bought the 122-square metre home in the coastal town of Torekov, together with Swedish TV producer and mother of his son Anna Eberstein.

But on Tuesday the Expressen tabloid reported that Grant has now handed in an application to the local authority in Båstad municipality to have the property completely demolished.

"I don't know if he's going to tear it down, but he has all opportunities in the world. He can afford to do what the heck he wants, six million [kronor] to him is probably like buying a couple of litres of milk," Martin Ploman, whose family had owned the property for 50 years before selling it to the actor on October 15th, told the newspaper.

"The only thing I hope is that he likes it and that it will turn out well," he added.

Grant had a son with Eberstein, the daughter of Swedish Social Democrat politician Susanne Eberstein, in 2012. It was reported last month that the pair are expecting a second child.

"I don't think he is going to come here to show off and be noticed by building some kind of huge bungalow with swimming pools and the like. But they are expecting their second child and it's a big garden where you can put up swings and stuff," said Ploman.

READ ALSO: Five questions before buying a home in Sweden

Documents shown to The Local last week confirming the sale.

Torekov is a seaside resort close to Båstad, one of the glitziest spots in Sweden, which hosts the Swedish Open tennis tournament each year. But although the town is already home to a number of celebrities, local residents seem less than impressed about news of the purchase.

"He has been here many times before, over several years. So it's not a big deal that he has bought a house here now," Anette Bohlin, 58, told The Local last week, revealing that Grant "bought cinnamon buns at the local cafe here every day last summer".

Other well known residents are understood to include Swedish singer Meja, who had a global hit in 1998 with the song 'All 'bout the Money', Swedish businessman Bertil Hult, and national football hero Henrik Larsson.

Hugh Grant already has two other children from his relationship with Tinglan Hong. His daughter Tabitha was born in 2011, while Felix was born a year later.

The actor is not the first celebrity to demonstrate his love for Sweden in recent months.

In May, US rapper Wyclef Jean revealed that he fell in love with Sandviken in central Sweden after a gig there and was planning a move to the town in the next couple of years.

Comments

See Also

The Local was last week able to reveal official paperwork confirming that the Hollywood actor had bought the 122-square metre home in the coastal town of Torekov, together with Swedish TV producer and mother of his son Anna Eberstein.

But on Tuesday the Expressen tabloid reported that Grant has now handed in an application to the local authority in Båstad municipality to have the property completely demolished.

"I don't know if he's going to tear it down, but he has all opportunities in the world. He can afford to do what the heck he wants, six million [kronor] to him is probably like buying a couple of litres of milk," Martin Ploman, whose family had owned the property for 50 years before selling it to the actor on October 15th, told the newspaper.

"The only thing I hope is that he likes it and that it will turn out well," he added.

Grant had a son with Eberstein, the daughter of Swedish Social Democrat politician Susanne Eberstein, in 2012. It was reported last month that the pair are expecting a second child.

"I don't think he is going to come here to show off and be noticed by building some kind of huge bungalow with swimming pools and the like. But they are expecting their second child and it's a big garden where you can put up swings and stuff," said Ploman.

READ ALSO: Five questions before buying a home in Sweden

Documents shown to The Local last week confirming the sale.

Torekov is a seaside resort close to Båstad, one of the glitziest spots in Sweden, which hosts the Swedish Open tennis tournament each year. But although the town is already home to a number of celebrities, local residents seem less than impressed about news of the purchase.

"He has been here many times before, over several years. So it's not a big deal that he has bought a house here now," Anette Bohlin, 58, told The Local last week, revealing that Grant "bought cinnamon buns at the local cafe here every day last summer".

Other well known residents are understood to include Swedish singer Meja, who had a global hit in 1998 with the song 'All 'bout the Money', Swedish businessman Bertil Hult, and national football hero Henrik Larsson.

Hugh Grant already has two other children from his relationship with Tinglan Hong. His daughter Tabitha was born in 2011, while Felix was born a year later.

The actor is not the first celebrity to demonstrate his love for Sweden in recent months.

In May, US rapper Wyclef Jean revealed that he fell in love with Sandviken in central Sweden after a gig there and was planning a move to the town in the next couple of years.

Join the conversation in our comments section below. Share your own views and experience and if you have a question or suggestion for our journalists then email us at [email protected].

Please keep comments civil, constructive and on topic – and make sure to read our terms of use before getting involved.

Please log in here to leave a comment.