Here's what Sweden's banknotes looked like 100 years ago

Sweden may be on its way to becoming a cashless society, but historical examples of its currency offer an interesting insight into the country's history.

The ten-kronor note hasn't existed in Sweden for more than 20 years, but at one point there were dozens of different designs for the note, with the country's different banks each designing their own.

Sweden's Royal Coin Cabinet museum has shared images of late 19th-century ten-kronor notes as part of an initiative to raise awareness of its collection.

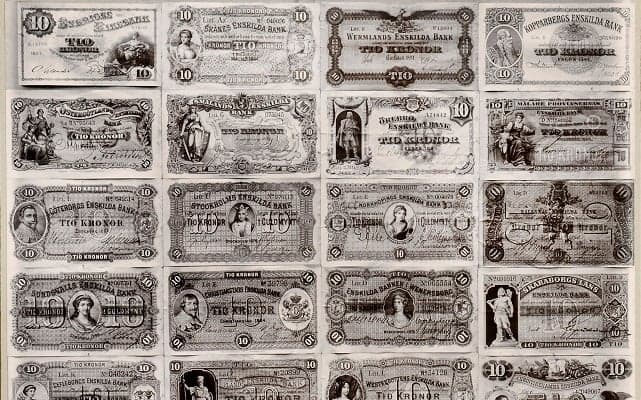

At the time, there were 31 private banks across the country, each of which had the power to issue its own banknotes, so in 1901, for example, there were 28 examples of the ten-kronor note. Banks would display images of all the valid notes, as seen in the picture above, so staff could carry out their jobs and spot forgeries.

"This was a special period in Sweden's economic history, where we had a standard currency but different banknotes," Åsa Hallemar from the museum told The Local.

"You can see that the motifs on the banknotes were there to promote the regions, for example people and buildings which were important to the city in some way."

READ ALSO: Cashless Swedes still sitting on old kronor worth billions

The below image of a ten-kronor note produced by Örebro Enskilda Bank in 1896 shows the city's iconic castle and a statue of nobleman Engelbrekt Engelbrektsson, who led a rebellion against Eric of Pomerania, which was in Örebro's main square.

Photo: Royal Coin Cabinet

Photo: Royal Coin Cabinet

The 1884 ten-kronor note from Kristinehamns Enskilda Bank depicts Queen Kristina, who founded the city Kristinehamn and gave it its name.

Photo: Royal Coin Cabinet

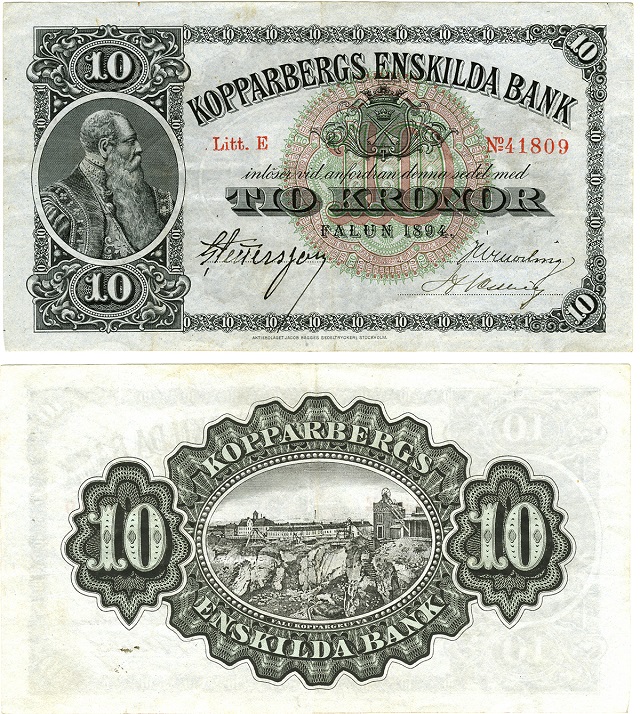

And an 1894 note issued by Kopparbergs Enskilda Bank in Falun has an image of the copper mine for which the area was well known, and King Gustav Vasa who also had a connection to the region.

Photo: Royal Coin Cabinet

The Riksbank, Sweden's central bank and the third oldest bank in operation, was established in 1668, but it didn't gain the exclusive right to issue banknotes until well over 200 years later.

This went some way in solving the problem of forgeries, which were frequent and often hard to spot with so many different versions of the bank notes in circulation simultaneously.

Comments

See Also

The ten-kronor note hasn't existed in Sweden for more than 20 years, but at one point there were dozens of different designs for the note, with the country's different banks each designing their own.

Sweden's Royal Coin Cabinet museum has shared images of late 19th-century ten-kronor notes as part of an initiative to raise awareness of its collection.

At the time, there were 31 private banks across the country, each of which had the power to issue its own banknotes, so in 1901, for example, there were 28 examples of the ten-kronor note. Banks would display images of all the valid notes, as seen in the picture above, so staff could carry out their jobs and spot forgeries.

"This was a special period in Sweden's economic history, where we had a standard currency but different banknotes," Åsa Hallemar from the museum told The Local.

"You can see that the motifs on the banknotes were there to promote the regions, for example people and buildings which were important to the city in some way."

READ ALSO: Cashless Swedes still sitting on old kronor worth billions

The below image of a ten-kronor note produced by Örebro Enskilda Bank in 1896 shows the city's iconic castle and a statue of nobleman Engelbrekt Engelbrektsson, who led a rebellion against Eric of Pomerania, which was in Örebro's main square.

Photo: Royal Coin Cabinet

The 1884 ten-kronor note from Kristinehamns Enskilda Bank depicts Queen Kristina, who founded the city Kristinehamn and gave it its name.

Photo: Royal Coin Cabinet

And an 1894 note issued by Kopparbergs Enskilda Bank in Falun has an image of the copper mine for which the area was well known, and King Gustav Vasa who also had a connection to the region.

Photo: Royal Coin Cabinet

The Riksbank, Sweden's central bank and the third oldest bank in operation, was established in 1668, but it didn't gain the exclusive right to issue banknotes until well over 200 years later.

This went some way in solving the problem of forgeries, which were frequent and often hard to spot with so many different versions of the bank notes in circulation simultaneously.

Join the conversation in our comments section below. Share your own views and experience and if you have a question or suggestion for our journalists then email us at [email protected].

Please keep comments civil, constructive and on topic – and make sure to read our terms of use before getting involved.

Please log in here to leave a comment.