Unique medieval Venetian coin found in abandoned Swedish port

Richard Orange - [email protected]

Published: 4 Sep, 2018 CET.

Updated: Tue 4 Sep 2018 11:35 CET

Archaeologists in Sweden have discovered a gold ducat from early medieval Venice in Elleholm, a once thriving port that has now entirely disappeared.

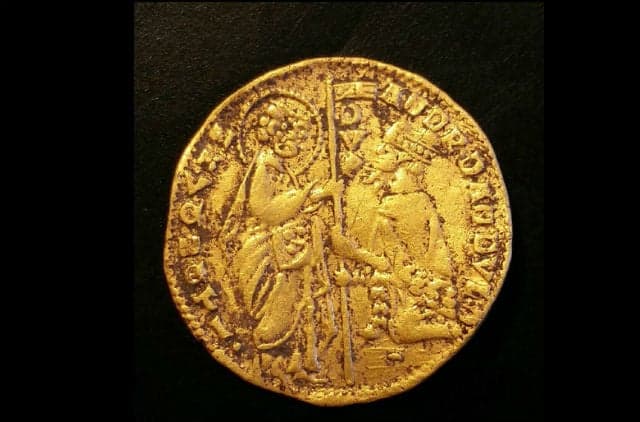

The ducat was minted during the reign of Doge Andrea Dandalos, who ruled the powerful Italian city state from 1343 to 1354.

"To find the first coin ever found in Sweden from the medieval Venice here, suggests it was an international trading port," Marcus Sandekjer, head of Blekinge Museum, told The Local.

The Archbishop of Lund controlled the city from 1450 right up until the reformation in 1536, when it was passed to the Swedish crown.

"Of course when you find coins from Italy in the Archbishop's city, it's tempting to think that it has something to do with ties to Italy and to the Pope," Sandekjer said. "But that is just a hypothesis."

On one side of the coin there is an image of St Marcus passing over a standard to the Doge, and on the other there is an image of the prophet Jesus Christ surrounded by an almond-shaped aureole of light, or Mandorla.

The city once took up most of the Elleholm island in the middle of the Mörrumsån river in Blekinge, and included the Sjöborg castle and a church.

"It's a fascinating place, just imagine this little city on an island in the middle of a river," Sandekjer said. "It was very compact."

The city was destroyed at least twice, once in 1436 during the Engelbrekt rebellion against the Kalmar Union, and once in 1524 during Søren Norby's Scanian rebellion.

The ongoing dig, a collaboration between the Blekinge Museum and Kulturen, a folk history museum in Lund, is the first on the site since 1924.

The city's disappearance has been linked to the Reformation, which stripped the Archbishop of most of his power, as well as to the development of the nearby port of Karlshamn, and to the changing requirements for a successful trading port.

"This is a small island in the river, upstream, which means they could never go in with ships to the actual island," Sandekjer explained. "It's a medieval solution for a city to put it upstream."

As trading volumes increased, ports moved directly to the sea, he said.

Sandekjer said a dendrochrological study of the remains of the bridge to the island had dated it back to 1340, indicating that the site had hosted a port for at least 100 years before it was formally granted city status.

The archaeologists have also found a lead seal from Flanders, dating to the first half of the 14th century.

"It was probably a seal for cloth or clothing," Sandekjer says. "So that shows us that it was an active place before we knew that it was active."

Comments

See Also

The ducat was minted during the reign of Doge Andrea Dandalos, who ruled the powerful Italian city state from 1343 to 1354.

"To find the first coin ever found in Sweden from the medieval Venice here, suggests it was an international trading port," Marcus Sandekjer, head of Blekinge Museum, told The Local.

The Archbishop of Lund controlled the city from 1450 right up until the reformation in 1536, when it was passed to the Swedish crown.

"Of course when you find coins from Italy in the Archbishop's city, it's tempting to think that it has something to do with ties to Italy and to the Pope," Sandekjer said. "But that is just a hypothesis."

On one side of the coin there is an image of St Marcus passing over a standard to the Doge, and on the other there is an image of the prophet Jesus Christ surrounded by an almond-shaped aureole of light, or Mandorla.

The city once took up most of the Elleholm island in the middle of the Mörrumsån river in Blekinge, and included the Sjöborg castle and a church.

"It's a fascinating place, just imagine this little city on an island in the middle of a river," Sandekjer said. "It was very compact."

The city was destroyed at least twice, once in 1436 during the Engelbrekt rebellion against the Kalmar Union, and once in 1524 during Søren Norby's Scanian rebellion.

The ongoing dig, a collaboration between the Blekinge Museum and Kulturen, a folk history museum in Lund, is the first on the site since 1924.

The city's disappearance has been linked to the Reformation, which stripped the Archbishop of most of his power, as well as to the development of the nearby port of Karlshamn, and to the changing requirements for a successful trading port.

"This is a small island in the river, upstream, which means they could never go in with ships to the actual island," Sandekjer explained. "It's a medieval solution for a city to put it upstream."

As trading volumes increased, ports moved directly to the sea, he said.

Sandekjer said a dendrochrological study of the remains of the bridge to the island had dated it back to 1340, indicating that the site had hosted a port for at least 100 years before it was formally granted city status.

The archaeologists have also found a lead seal from Flanders, dating to the first half of the 14th century.

"It was probably a seal for cloth or clothing," Sandekjer says. "So that shows us that it was an active place before we knew that it was active."

Join the conversation in our comments section below. Share your own views and experience and if you have a question or suggestion for our journalists then email us at [email protected].

Please keep comments civil, constructive and on topic – and make sure to read our terms of use before getting involved.

Please log in here to leave a comment.