Published: 20 Sep, 2022 CET.Updated: Sat 15 Jul 2023 13:42 CET

Detached houses (villor) in Enskede, Stockholm. Photo: Fredrik Sandberg/TT

Interest rate rises are putting the squeeze on consumers in Sweden. Here's how you can get some relief if you are struggling to make your monthly mortgage payments.

Advertisement

How high are interest rates now?

Sweden's Riksbank Central Bank at the end of June raised the repo rate or key interest rate to 3.75 percent, up from 3.5 percent at the last hike in April.

Advertisement

What help can you get?

Sweden's Financial Supervisory Authority in a press release in September 2022, when rates were raised to 1.75 percent, published a Q&A on its website to inform consumers of the possibility of getting excused the mandatory amortisation payments in Sweden.

"If it gets tight, it's best to ring your bank and start a dialogue," he said. "They are used to handling this sort of question. You should not be afraid to ring."

"A lot of households are going to find this really tough, and this is hopefully only a temporary problem, so if you have a problem as a household, you should talk with your bank. We think it's good if people take advantage of this."

Advertisement

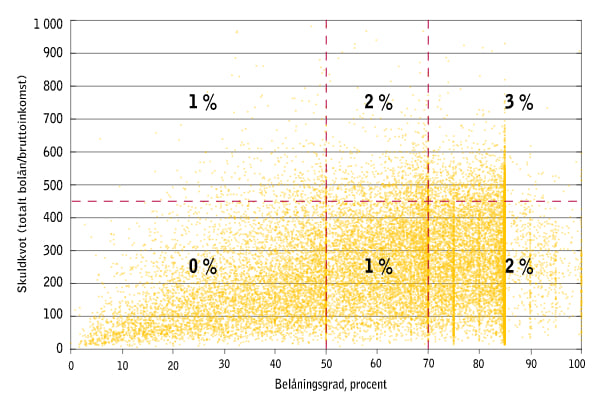

What is Sweden's amorteringskrav system to reduce interest-only mortgage payments?

Sweden in 2016 tried to lower the risk in its housing market, by bringing an end to interest-rate only mortgage payments for anyone taking out loans worth more than 50 percent of the property's value, or borrowing more than 4.5 times their annual income.

This means you must pay down between one percent and three percent of your loan every year, depending on how big a share of your annual income or how big a share of the value of the property you have borrowed.

You can see this in the graph below, where skuldkvot refers to the size of your loan compared to your annual income, and belåningsgrad refers to the size of your loan as a percentage of the value of your property.

Those who have borrowed less than 50 percent of the value of their home, with this loan less than 4.5 times their annual income, don't need to pay anything back, while those borrowing more than 70 percent who have borrowed more than 4.5 times their annual income must pay off three percent of their mortgage per year.

Source: Financial Inspection Authority of Sweden

If I can't afford to pay off my mortgage, what should I do?

According to the rules of the amorteringskrav, mortgage lenders are allowed to temporarily excuse borrowers from the requirement to pay off between one and three percent their mortgage principal - effectively the amount you have borrowed and have to pay back.

The decision on whether to excuse a borrower is taken by banks on an individual basis, and requires only that the borrower declare a "special reason".

Advertisement

What might a "special reason" be?

A special reason would be if a household's economy is "significantly worsened". The Financial Supervisory Authority suggests that this might be because a member of the household is sick or unemployed, or if household finances have been appreciably worsened by "increased costs", such as the higher electricity bills seen last winter.

A "special reason" can only be something which happens after a mortgage has been granted, and it should be something which could not have been foreseen at the time the mortgage was agreed.

The authority stresses that a rise in the repo interest rate would not normally be enough to count as a "special reason".

"That a household is sensitive to rate rises and is affected when the mortgage rate is increased is not in itself a "special reason".

It said that in recent years banks are supposed to set their mortgages so that lenders can handle interest rates of between 5 and 6 percent, considerably above the roughly 4 percent mortgage rate most borrowers will experience after the September 21 rate rise.

However, for those who took out their mortgages before key interest rates started to increase, who had their loans approved on a hypothetical max rate of between 5 and 6 percent, may be eligible for a temporary pause in payments if this is combined with some other increased unforeseen cost which has occurred at the same time.

More

Comments

Join the conversation in our comments section below. Share your own views and experience and if you have a question or suggestion for our journalists then email us at [email protected].

Please keep comments civil, constructive and on topic – and make sure to read our terms of use before getting involved.

Source: Financial Inspection Authority of Sweden

Source: Financial Inspection Authority of Sweden

Join the conversation in our comments section below. Share your own views and experience and if you have a question or suggestion for our journalists then email us at [email protected].

Please keep comments civil, constructive and on topic – and make sure to read our terms of use before getting involved.

Please log in here to leave a comment.